It Ain't So, Alan! Why Greenspanian Central Banking Is the Mortal Enemy of Capitalist Prosperity

October 20, 2018

abundantly clear by his pronouncement on CNBC regarding the current labor market:

“Tightest labor market I’ve ever seen.” – Greenspan onAs an empirical matter, of course, that’s rank nonsense – and is among the stupidest quips the Maestro has ever uttered. That’s because the law of supply and demand dictates that if the labor market is actually the tightest since Greenspan began his career in the 1950s, wage rates should also be rising at the highest rate ever.@CNBC

In fact, at 2.8% year-year-over year for September 2018, nominal wage growth (red line) is the lowest it’s been since the late 1960s; and in real terms, the story is even worse.

To wit, between 1955 and 2000, real compensation per hour grew at a 1.75% annual rate – and that’s the average across seven business cycle, including recession years.

By contrast, we are now at the top of the second longest business expansion in history, and real compensation (purple line) was up just 0.7% over the past 12 months. And that’s virtually the weakest late cycle growth rate on record.

In short, the only valid free market measure of “tight” is the price of labor, and those limpid wage rates say absolutely not.

Trumped! A Nation on t...

Best Price: $3.17

Buy New $26.00

(as of 05:40 EDT - Details)

Trumped! A Nation on t...

Best Price: $3.17

Buy New $26.00

(as of 05:40 EDT - Details)

Of course, what the Maestro and his Keynesian fellow travelers

refer to is not the verdict of the marketplace, but bureaucratic

guesstimates about labor market conditions published monthly by the BLS.

Yet it doesn’t take even 10 minutes worth of investigation to show that

the BLS’ tightness gauge – the U-3 unemployment rate – is not worth the

paper it’s printed on.

Of course, what the Maestro and his Keynesian fellow travelers

refer to is not the verdict of the marketplace, but bureaucratic

guesstimates about labor market conditions published monthly by the BLS.

Yet it doesn’t take even 10 minutes worth of investigation to show that

the BLS’ tightness gauge – the U-3 unemployment rate – is not worth the

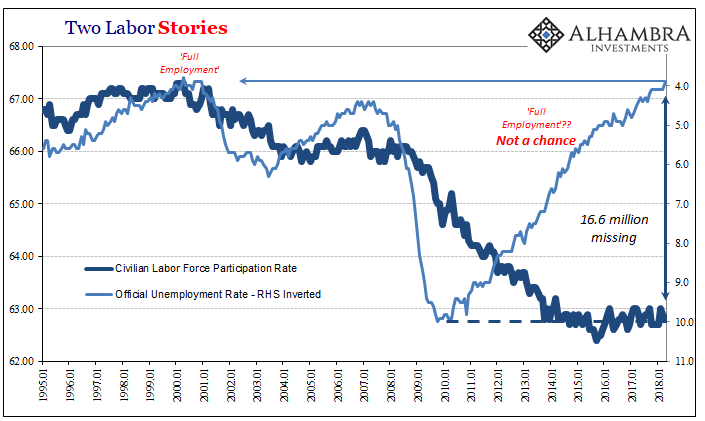

paper it’s printed on.As Jeff Snider has cogently demonstrated, we are at 3.7% unemployment only because the labor force participation rate as measured by the BLS has plunged.

In fact, at the same 3.7% so-called full employment rate which pertained when the Maestro was riding high in the late 1990s, the labor force participation rate was north of 67%, not today’s 62.7% (September). And that means the Maestro’s alleged labor shortage rests on the back of 16.6 million workers who have purportedly gone missing!

We don’t think any workers have actually gone missing at all, and believe that the actual unemployment rate is upwards of 40%, as demonstrated below. But suffice it to say here that there is a reason why Wall Street and Washington economists alike insist on using the patently ridiculous and grossly erroneous numbers manufactured by the BLS data mills.

To wit, the BLS jobs data – and especially the U-3 unemployment rate – function as a convenient “help wanted” sign for Keynesian interventionists. The implication is that the free market’s pricing system for labor, goods and services doesn’t work very well, and that the wise guiding hand of the state is needed to regulate an economic ether called “aggregate demand”.

That is to say, the US economy resembles a giant economic bathtub, and the aim of government policy is to keep it filled exactly to the brim. That way, everybody’s got a job, a good wage, a nice life, no (inflation) worries and perhaps is even rid of sniffles and hangnails, too!

So when the U-3 unemployment rate is at 11%, 8% or 5%, there is purportedly a large deficiency of demand, signaling that the state and its central banking branch need to pump more spending into the bathtub via fiscal or monetary stimulus.

Likewise, when U-3 reaches the alleged “full employment” rate at +/- 3.7% that’s a signal the tub is close to full and that interest rates need to be raised in order to curtail credit expansion and spending, thereby insuring that an inflationary overflow does not upset the macroeconomic applecart.

But here’s the thing. The 12 members of the FOMC might as well be standing out on Independence Avenue waving their arms in order to keep marauding elephants from overrunning the Eccles Building!

That’s about how useful U-3 is as a measure of labor market or macroeconomic conditions; and it’s also about as worthless as is the Fed’s endless pegging of money market rates and massive intrusion in the bond markets in furtherance of capitalist prosperity.

The fact is, the potential labor supply from both domestic and offshore sources is so limitless that the only thing needed to mobilize more employed hours is the pricing system, not the monetary politburo’s (FOMC) machinations in the financial markets.

At a high enough wage rate, you will get housewives out of the kitchen, students off their duffs, more volunteers for overtime, and, if need be, more peasants out of the Chinese or Vietnamese rice paddies. In today’s globally networked, traded and welfare-enabled world, there will never be a physical shortage of labor hours – just the right price to bring latent hours into monetized production.

Needless to say, the latent hours now sequestered in Federally subsidized basket-weaving classes or playing shuffleboard on early retirement or disability do raise market-clearing wage level s at the margin. But you can solve that problem but cutting welfare benefits, not giving the Fed a mandate to fiddle with interest rates and financial asset prices.

That latter only fosters increasingly destructive gambling, bubbles and malinvestments in the financial system, not higher production, employment and prosperity on main street.

The Great Deformation:...

Best Price: $2.35

Buy New $10.70

(as of 03:50 EDT - Details)

The Great Deformation:...

Best Price: $2.35

Buy New $10.70

(as of 03:50 EDT - Details)

Indeed, there is no need for central bankers at all when it comes to economic growth, jobs, incomes and prosperity. That’s because Say’s Law is as valid today as it has always been.

Work, effort, production and enterprise are what create both current income and future growth. Demand flows from supply and spending flows from income; capitalism doesn’t need any U-3 obsessed central bankers to make it all happen.

Likewise, the labor pricing system in a $20 trillion economy has it hands down over the 12 PhDs, bankers and Washington apparatchiks who sit on the FOMC. If the market is heavy with latent labor hours, real wage rates will come down; and if it’s light, real wage rates will rise sufficiently to attract the needed hours.

In fact, now that most of the monopoly industrial unions have been broken or defanged – even the old Keynesian saw about “sticky” wages is self-evidently inoperative. The truth is, there is nothing about the contemporary labor market that requires the helping hand of the Fed at all.

Moreover, there is no even theoretical possibility of runaway wage inflation of the type that industrial unions led by the UAW and Steelworkers were able to generate in the late 1960s. That because virtually every manner of goods produced in the US economy and a growing portion of services can now be supplied from offshore, and often at far lower wage rates – even adjusted for productivity and transportation – than paid by domestic suppliers.

That is to say, the only semblance of an inflation problem facing the US economy is the roaring inflation of financial asset prices, which is the Fed’s stock and trade.

So if you want to have honest full employment and maximum possible capitalist prosperity, unleash the free market and the pricing system for goods and labor; and if you want to avoid inflation of all types – goods, services, credit and stock prices – abolish the FOMC, which causes it.

Needless to say, reversion to Carter Glass’ original Fed design as a “bankers’ bank” empowered to discount and liquefy sound commercial credits (real bills), and one which had no macroeconomic remit whatsoever, would put today’s masters of the universe out of business.

In fact, the Glassian Fed only needed to employ green eyeshades who knew how to read financial statements and assess credit risk on business loans offered as collateral at the Fed’s discount windows. PhD economists and policy apparatchiks bent on improving the work of labor and entrepreneurs on the free market need not have even applied.

Stated differently, if the BLS didn’t exist – and it surely is not needed for true prosperity – Keynesian central bankers would have to invent it. It is the BLS’ phony labor market gauges (and price indices, too) which provide the fodder to justify the destructive full-employment focussed make-work of central bankers.

Ironically, the Maestro’s risible assertion this AM about the tightest labor market in modern history does nothing less than underscore that the the whole BLS employment/unemployment reporting framework and model is essentially a pile of garbage; it might have been relevant during the days of your grandfather’s economy, if even then, but is a crock in today’s world drowning in available labor.

So let us remind once again:The BLS data is built on the flawed notion that labor inputs can be accurately measured by a unit called a “job” and that an economic trend in motion tends to stay in motion.

To the contrary, in today’s world labor is procured by the hour and by the gig – meaning that the “job” units counted in both the establishment and household surveys are a case of apples, oranges and kumquats. The household survey, for example, would count as equally “employed” a person holding:

- a 10-hour per week gig with no benefits;

- a worker holding three part-time jobs adding to less than 36 hours per week with some benefits; and

- a 50-hour per week manufacturing job (with overtime) providing a cadillac style benefit package.

In short, the monthly jobs report is not an accurate empirical snapshot of where the real world labor market actually is; it’s a modeled projection of where the BLS bureaucrats and their Keynesian tutors think it should be.

And that’s also why the BLS “jobs” confection is useless at turning points in the business cycle. During the 2008-2009 employment collapse, for instance, it initially over-reported the nonfarm payrolls by nearly 500,000 jobs per month because it assumed the previous trend was still in motion – even as employers were throwing workers overboard with reckless abandon after the Lehman meltdown on Wall Street.

The Triumph of Politic...

Best Price: $2.54

Buy New $8.45

(as of 05:05 EDT - Details)

The Triumph of Politic...

Best Price: $2.54

Buy New $8.45

(as of 05:05 EDT - Details)

Aside from cyclical turning points (mostly triggered by the Fed itself), the larger context is this: The natural tendency of a capitalist economy is to expand if the work force is growing and if the state does not excessively retard investment and productivity growth.

Those natural expansionary forces have been at work in tepid form since the recessionary correction of 2008-2010. They account for the “recovery” of some 8.5 million jobs which were lost in the Great Recession and the modest incremental gains that have been generated since break-even was achieved in 2014.

But what is important is the growth rate of actual labor units employed and the relationship of that to the available potential labor force – not simply the BLS “jobs” model. The latter basically floats on the back of the natural capitalist business cycle expansion and enables the monetary politburo in the Eccles Building to claim credit for what are really nothing more than statistical proxies.

Needless to say, we think there is a far more insightful and accurate way to look at labor utilization and to assess whether or not an Awesome state of affair has actually been achieved.

As we indicated above, back in the year 2000 (the last time U-3 hit 3.7%) what we consider to be the comprehensive unemployment rate was 34.6%. Today it stands at 40.0%.

Since the turn of the century, therefore, there has been enormous deterioration in the US economy’s use of its potential labor supply. Yet as the Baby Boom rapidly ages and the Welfare State burden soars, that is a very bad thing.

Stated differently, the US has not utilized the last 9 years of so-called recovery to get back to Awesome – as implied by the BLS reports and Alan Greenspan’s “tightest” ever labor market pronouncement.

Instead, it has wasted a crucial decade in front of the Baby Boom retirement bow-wave – continuing to peddle backwards with regard to its underlying capacity for economic growth and rising real incomes. If nothing else, the latter are absolutely essential to pay the taxes that will be needed to prevent the US Welfare/Warfare State from fiscally capsizing in the decades immediately ahead.

In this context, we measure the potential labor force as the US population 20-69 years of age and assume that in theory every adult could work 2000 hours per year in the monetized labor market.

That avoids the obvious problem in the BLS statistics with respect to work and activity relative to the official labor force and monetized economy. For example, the BLS counts three jobs for a two-earner family which hires a full-time housekeeper, but just one job for the same family where one spouse works in the monetized economy, one-stays home and neither hires a third person to do the home chores.

The same logic applies to the 30-year old still in graduate school living on Uncle Sam’s student loans versus holding a job in the monetized economy; or the former office worker on disability who got a bad back and corporal tunnel bending over a typewriter; or the 60% of able-bodied recipients on foods stamps who do not currently hold a job; or the millions of millennials in mom and pops basement who sell empty beer bottles on eBay.

Many factors drive whether potential labor hours get sequestered outside of the monetized economy in housework, studentdom, on the welfare rolls or in moms basement. But the interest rate on overnight funds is surely the least of them.

Nevertheless, all things equal under today’s demographic and fiscal circumstances requires that the comprehensive unemployment rate needs to be dropping – so that Uncle Sam can find the tax receipts needed to prevent a complete societal civil war a few years down the road.

But it’s not happening. In December 2000, there were 175.5 million adults aged 20-69 – meaning that the implied potential labor force amounted to 351 billion labor hour per annum. During that same month, the BLS measured 229.5 billion hours actually employed in the non-farm economy at an annual rate.

Accordingly, unemployment amounted to 121.5 billion hours or 34.6% of the potential available hours.

By contrast, the adult population 20-69 years of age is now 211.6 million and available hours total 423.2 billion per annum. Against that, the BLS most recent measure shows 254.2 billion hours actually employed – implying 169 billion unemployed labor hours and a 40.0% comprehensive unemployment rate.

Stated differently, between the two 3.7% anchor points on the U-3 unemployment during the last 18 years, the level of unemployed US labor has increased by 48 billion hours per annum, and the rate has risen commensurately.

More importantly, potential labor grew by 72 billion hours or at a 1.05% per annum rate during that period, while actually employed hours rose by only 25 billion and 0.58% per year.

And that’s exactly the skunk in the woodpile. By contrast, during the 1980 to 2000 peak-to-peak periods, the potential labor force grew by 2.2% per annum, and labor hours actually utilized rose by nearly an identical 1.9% annualized rate.

So we are now at the opposite end of Awesome and not even in the zip code of a labor shortage. In 1980, the Baby Boom was just beginning to flood into the labor force, and female participation rates in the monetized economy were rising rapidly; and those hours were put to work.

By contrast, employed hours have grown at only one-quarter that rate since December 2000 and the true (comprehensive hours based) unemployment rate has steadily risen.

The reason for that is not hard to find. Fed policy has badly damaged the main street economy via its massive inflationary incentive for off-shoring of high value production and jobs while turning the C-suites of corporate America into predatory dens of financial engineering.

At the same time, Welfare State policy has further drained labor resources from the monetized economy with massive increases in food stamp, disability, Medicaid and other welfare programs.

So if you want to fix the real labor market problem, remove the fiscal subsidies and incentives for keeping potential hours off the market.

But most importantly, abolish the FOMC. It’s the mortal enemy of capitalist prosperity.

Reprinted with permission from David Stockman’s Contra Corner.

No comments:

Post a Comment