Digital Currency: The End Of American Entrepreneurship & Small Business

Why Small Business Doesn’t Stand A Chance In The Neo-Bank Era

By Bill Sardi

September 4, 2020

“Permit me to issue and control the money of a nation,

and I care not who makes its laws.”

— Mayer Amschel Rothschild

They call it Fintech. It will abolish American entrepreneurship and obliterate small business enterprises.and I care not who makes its laws.”

— Mayer Amschel Rothschild

FINancial TECHnology that will rule over the lives of everyone on the planet, rich or poor, is due to be unleashed in January of 2021 under what the International Monetary Fund calls a GLOBAL RESET.

To make this happen, banks will be closing branches under the pretense its workers are quitting over

fear of transmission of the COVID-19 coronavirus from bank customer to bank teller. Intentional central bank induced inflation will crush the purchasing power of the American dollar. Then there will be pre-planned shortages of cash and coin that will force the public to beg for currency reform – the elimination of paper money and its replacement with a digital money card, what the World Economic Forum calls THE 4TH DIGITAL INDUSTRIAL REVOLUTION.

Beyond Blockchain: The...

Best Price: $23.95

Buy New $24.95

(as of 03:36 EDT - Details)

Beyond Blockchain: The...

Best Price: $23.95

Buy New $24.95

(as of 03:36 EDT - Details)

Digital money will be global, not just local. The poor (nearly 3/4ths of the people on Earth earn $10 a day or less) will perceive this “equity card” as evening-up the playing field. Kind of like everybody getting an American Express Platinum Card. Everybody can get credit and with collateral make loans, even a poor farmer in Africa. At least that is what the globalist bankers claim.

Making the public beg for a new currency

A report posted at Deutsche Welle (DW.com) states: “Worried about citizens abandoning central-bank-backed cash in favor of privately run digital currencies, the European Central Bank set up a task force. The aim is not to promote a digital euro per se but to be ready to issue it if citizens demand it.” Of course, no mention how the banksters are stealthily ushering in the demise of paper money and then plan to coerce the population to beg for relief with their digital alternative.

Fear of paper money

Slanted research studies (frankly, just plain propaganda) have already been spread to induce undue fear of paper money. The news media quotes studies which show banknotes host around 26,000 colonies of bacteria and human viral particles can “survive” on a banknote for up to 17 days, with one-dollar/five-dollar notes changing hands more than 100 times per year on average. That is the current coronavirus dogma.

This is nothing more than planted malarky as viruses are not alive and even the Centers for Disease Control now concedes the way viruses are spread to another human respiratory system is via airborne transmission from lung to lung, not by hand/surface contact.

While banknotes may harbor bacteria, no outbreaks of any disease have been linked with handling paper money. Only laboratory simulations make such a claim. An MIT report dismisses the idea paper money spreads infectious disease.

Facebook: Libra - GLOB...

Buy New $3.49

(as of 05:13 EDT - Details)

Facebook: Libra - GLOB...

Buy New $3.49

(as of 05:13 EDT - Details)

Regardless of these facts. The World Health Organization issued a warning (March 8, 2020) that handling paper money can spread the COVID-19 coronavirus. Businesses then began to shun paper money and insist upon debit/credit card purchases. The Brinks truck just went the way of the buggy whip.

If paper money did in fact play a role in the spread of respiratory viruses, that would not explain why cold, influenza and coronaviruses arise during winter when sunshine vitamin D levels are low. And bank tellers have not been identified as being any more ill than the rest of the population.

Brainwashing Americans

But we now live in a world of “fake news.” TV newscasters do the thinking for mindless spectator Americans. This is why Americans are frequently called “sheeple.” For example, Americans pointlessly wear face masks while driving when they are the only party in the car.

These patriotic to-a-fault Americans dutifully do as they are told and wear face masks even though there is no legislative mandate, forgetting the country was started by opposition to (British) authority.

Now that it has become apparent the COVID-19 coronavirus deaths were overstated by 80% to falsely heighten public fear and prep the masses to beg for vaccination, will Americans ever realize they have been conned?

The largesse of this scam created its believability. TV can instill misplaced fear like no other medium. The American public doesn’t quite understand, the fewer people who are infected the more who will need to be vaccinated. The news media parrots all of the pro-vaccine misinformation for public health agencies that have financial conflicts of interest.

Rigged: Exposing the L...

Best Price: $15.32

Buy New $14.96

(as of 05:13 EDT - Details)

Rigged: Exposing the L...

Best Price: $15.32

Buy New $14.96

(as of 05:13 EDT - Details)

Did you hear about the ATM machine that killed a baby?

There will be more and more reports planted in the news media that will frighten the public to fear paper money. Anticipate some fear-evoking story, like a mother who drove home after withdrawing money from a bank ATM machine and unknowingly infected her newborn baby who then died from an infectious disease that was caused by the very same pathogen found on the paper money that the child’s mother withdrew from the ATM machine. ATMs kill! The mother is also blamed for not vaccinating her infant child immediately after birth. This kind of made-up story would “kill two birds with one stone,” creating an unfounded fear of paper money and guilt over refusal to vaccinate.

Digital AI control

Little do Americans realize, the vanishment of paper money gives banks and government complete control over its citizenry. The World Economic Forum, the instigator of the COVID-19 coronavirus pandemic (sponsored Event 201 that was supposedly an exercise for the pandemic that was to come) wants to link the issuance of a digital currency card with clearance that a person has been vaccinated. Employers that don’t require their employees to undergo immunization will face having their digital currency card turned off.

It is well enough that people of the

nation do not understand our banking and monetary system, for if they

did, I believe there would be a revolution before tomorrow morning.

~ Henry Ford

False promises of helping the poor, women, and the unbanked~ Henry Ford

The hidden agenda behind the COVID-19 coronavirus pandemic is centered around abandonment of paper money and coin with forced substitution of digital currency that will falsely promise to help the poor and unbanked and make them more equal (and less racist) with the rest of the world.

The Zero Interest Trap

Best Price: $12.16

Buy New $19.00

(as of 05:13 EDT - Details)

The Zero Interest Trap

Best Price: $12.16

Buy New $19.00

(as of 05:13 EDT - Details)

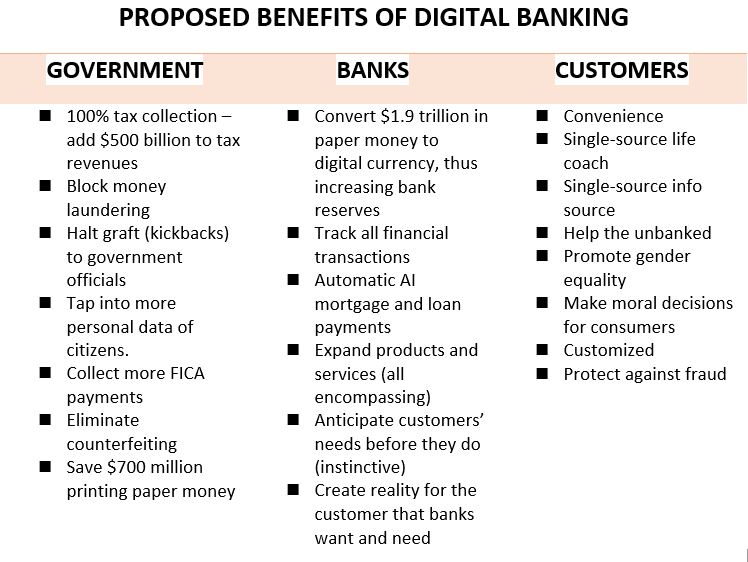

Ushered in under the guise it will speed payments, protect privacy, reduce costs, represent the unbanked and offer value-added services (health, transportation, education, food, an endless list of extra benefits), the global digital money card will be touted as the only alternative to another contrived crisis.

Proponents of digital banking point to a survey which shows 76% of respondents said “the economy of my country is rigged to advantage the rich and powerful.” Public sentiment may cause the public to prefer the digital card over paper money, especially among the poor who have no feeling they have any financial stake in America.

Digital banking will result in the end of local bank branches and globalize regulations so banks can become global, not local. Without paper money and coin, traditional bank branches will be abandoned, all financial transactions, personal and commercial, will be performed online or on the telephone – home loans, auto loans, etc.

Where are they taking us?

Bank branches as we know them today will no longer exist in the future. Banks used to be a place. Now they will only exist in electronic space.

MoneyWise says over 80% of US consumer spending was cashless in 2017. No more brick and mortar banks. Not even an ATM machine will be needed as currency and coin are no more. I have to repetitively make this point because it may be difficult for Americans to imagine this, given that banks are a part of the landscape of modern America. Here today, gone tomorrow, just like road maps that are now replaced by GPS and VHS video cassettes replaced by DVDs. But this is the physical vanishment of an entire American institution.

That safe looking building with Greek columns and a giant vault in your town is to be no more. Bank robbery would also be a crime of the past. Ironically, the public is all wearing face masks while the banksters are robbing us blind.

In 1995, billionaire philanthropist Bill Gates,

who founded the BETTER THAN CASH ALLIANCE said:

“Banks are dinosaurs, they can be bypassed.”

What is driving this change?who founded the BETTER THAN CASH ALLIANCE said:

“Banks are dinosaurs, they can be bypassed.”

Our Enemy, the State

Best Price: $9.84

Buy New $9.95

(as of 03:20 EST - Details)

What is the driver behind these rapid changes in banking? – – – Competition. Challenger banks are disrupting traditional banking models, rapidly making inroads into the sector’s profits by offering digitalized alternatives.

Our Enemy, the State

Best Price: $9.84

Buy New $9.95

(as of 03:20 EST - Details)

What is the driver behind these rapid changes in banking? – – – Competition. Challenger banks are disrupting traditional banking models, rapidly making inroads into the sector’s profits by offering digitalized alternatives.Alibaba and Google are moving into the loan business. Banks are going to compete with the likes of Amazon, Facebook and Apple… TechFins pose a bigger threat to banks than any other disruption.

A bank reform leader, Genpact, says: “Once Amazon knows more about me than my bank knows about me that becomes an existential challenge for banks.”

Genpact: “Banks will need to compete with the likes of Amazon on customer experience, while also offering something deeper, be it through relationships and service, boosting businesses and communities, or taking a stand on global issues to engender trust…. Banks will transition from offering financial services to enabling financial betterment.” Of course, the definition of betterment will be themselves, not the banking public.

____________________________________________

Mark Carney, Governor of The Bank of England,

offers a contrarian position:

offers a contrarian position:

“Many citizens in advanced economies

are facing heightened uncertainty, lamenting a loss of control and

losing trust in the system. Rather than a new golden era, globalization

is associated with low wages, insecure employments, stateless

corporations and striking inequalities.”

____________________________________________Managed by AI (automated intelligence)

Genpact poses itself to be an answer to these problems with what it calls “optimized reality, ethical impact and whole-system planning.” GenPact says banks will even use automated intelligence (AI) to determine the mood of their customers and then tailor programs and experiences around those mental frameworks.

The Coming Cashless So...

Best Price: $2.25

Buy New $45.01

(as of 01:05 EST - Details)

The Coming Cashless So...

Best Price: $2.25

Buy New $45.01

(as of 01:05 EST - Details)

The banks will be so tech-driven that an article in Global Finance Magazine says “the bank of the future could even, conceivably, be led by a robot CEO. It will be AI driven.” How do you fire a robot? How do you sue a robot?

Banks will use AI to become instinctive, says Genpact, to know what customers need before they themselves do. In other words, do the forward thinking for them.

Big business moves in on small business enterprises

GenPact pretends the new neo-banks will “enable people and businesses.” In reality, neo-banks will destroy entrepreneurship and small business. Neo-banks will not just expand into offering safer investment products, they intend to expand into every industry, health, medicine, food, auto, travel, insurance, vitamins, even dog shampoo services.

Like Amazon and Facebook are now doing, these neo-banks will begin to create their own covert brands. Order vitamin pills at Amazon today and all of Amazon’s own private-labelled brands are ranked at the top of the order page and given outstanding customer reviews. Amazon and Facebook steal business from their own vendors who post-up products for sale at Amazon.

For example, bankers will add cell phone apps to monitor blood pressure, body temperature, pulse rate, and then AI will book appointments with doctors, and the public will be reminded to vaccinate against the flu, and take their medicines on time.

Now, if you have high blood pressure and you order a pizza with double meat and cheese, the AI-driven digital money card may balk, knowing that is not best for your health. Remember this audio scenario that was created over a decade ago?

(Click to view) ORDERING A PIZZA IN THE FUTURE

An unspoken objective of the COVID-19 lockdown has been to force

small businesses out of operation. Soon neo-banksters are going to

control everything, from buying a house, to scheduling a massage and

being reminded you need booster flu shots. There isn’t going to be any

small business left.

Conspiracy Theories: S...

Buy New $2.99

(as of 05:13 EDT - Details)

Conspiracy Theories: S...

Buy New $2.99

(as of 05:13 EDT - Details)

Just how will neo-banks, that are putting so many people out of business, thrive off of consumers who have been displaced from their jobs and are living on guaranteed income payments from the government? Of course, these payments will be directly placed on the digital equity card.

As an aside, the US Gross Domestic Product (GDP) is headed to being a measure of welfare rather than productivity. Can you imagine?

Social scoring

Neo-banks will do all this under the banner of being inclusive – promoting gender equality, sustainability, and penalize customers who purchase goods or services from companies who don’t have a good “planet score.” The bank will be making “moral decisions” in place of customers who are supposed to do that. The bank’s world view (Green New Deal, climate change, global warming) will be forced on its depositors.

Advocates of digital money point to The People’s Bank of China that has ability to monitor Digital Currency Electronic Payments (DCEP) transactions and “can help improve the efficacy of monetary and fiscal policy operations as well as make it easier to fight financial crimes including money laundering and the financing of terrorism. Monitoring monetary transactions via digital currency will significantly strengthen the Chinese government’s social credit scoring system, used to control its citizens by reward or punishment of certain behaviors. Basically, the more citizens that use DCEP instead of physical cash, the more the government can monitor and control their lives,” says a report posted by the Atlantic Council.

You’ll trust the banker who you think knows you

Staying connected and building accumulated experiences will foster trust with the customer and will be the doorway for banks to offer all these added products and services that today are outside of a traditional bank’s menu.

Here is the way bankers explain it: “If you’re playing Taylor Swift’s latest hits on the Amazon Alexa (voice-activated assistant), the next step is probably, ‘Alexa, buy this album’; and then it’s not long before you’re saying, ‘Alexa remortgage my house’,” says a report in Global Finance Magazine.

Benefits accrue to governments, FinTechs

What FinTech appears to be offering is banking on a bankers’ terms, not the public’s terms. The greater benefits accrue to government and the banksters in a digital money system.

Benefits for government

Government is going to love digital money. A switch from paper to digital money means hundreds of billions of dollars of increased tax revenues for the federal government. Digital money brings more income-earning activities out from the shadows and into the taxable income column. The IRS estimates the US lost $500 billion in tax revenues in 2012 due to unreported income. Now 100% of that will be reported and appropriately taxed.

Then there is an obvious savings from not having to print billions of bank notes each year – a savings of ~$700 million/year.

Another benefit derived from digital money is inherent invulnerability to counterfeiting. However Central Bank Digital Currency (CBDCs) could, via hacking, put money at risk for electronic counterfeiting on a more massive scale. Security systems will have to be airtight.

The benefits of digital banking are huge for banksters

According to Genpact, a company that is fashioning transition of brick and mortar banks to digital banks, the banking industry spends $270 billion on compliance costs and 10-15% on governance, risk management and training its workforce. Much of these expenses will be eliminated, including thousands of bank jobs. There are ~472,000 bank tellers in the US who may soon be job hunting.

Added benefit to bankers

As of August 5, 2020, there was $1.95 trillion worth of Federal Reserve notes in circulation. The public will likely be given an expiration date for this paper money. If all these predicted events go down, let’s hope our paper money is converted to digital at a 1-to-1 value. Then there is another $500 billion in US paper money overseas that will need to be repatriated. The banks will now be automatically buoyed by $1.95 trillion + $500 billion of added reserves.

Negatives for consumers

Bank depositors will benefit from a digital money card, but only in small ways. Glen Frost, Founder; FinTech Summit & FinTech Awards explains that FinTechs typically offer “better user experience, cheaper prices and a dedicated focus on solving a specific problem.” But these small savings won’t elevate any American’s income bracket by any measure. The benefits to consumers from the digital neo-dollar will be marginal. Bankers’ objective is to make everyone a debt slave.

In foreign trade, the US dollar is used as the currency of exchange. “A sovereign digital currency” is posed as an effective alternative to the U.S. dollar settlement system.” There wouldn’t be as much forced demand for the US dollar and its value would likely drop in international trade. Then foreign-made goods would cost more.

Digital central banks can also impose negative interest rates on holders of digital money, something a central bank cannot do with cash. This represents confiscation of money.

Another drawback is that Digital Electronic Currency Payments (DCEP) take away the anonymity of cash transactions, reducing personal privacy and handing the government a powerful tool to monitor and control its citizens. The IRS knows how much money your earned and how much you spent, but now it is going to know where every dime went.

Cash-based businesses are toast

It’s all over for cash-based businesses (street vendors, restaurants, lawn services, babysitters, laundromats, vending machines, ice cream trucks) who are already being “disintermediated.” Vending machines and laundromats will have to re-tool. Even street beggars are out of business.

It has also been suggested that the Digital Electronic Currency Payments (DCEP) that come along with digital currency can be used for international payment transactions, especially as an alternative to the SWIFT system that handles wire transfer of funds.

Digital money and the disappearance of paper money is inevitable

Plans are already underway. The Federal Reserve has announced it is building and testing a hypothetical digital currency, equivalent of cash. God knows, government probably has a digital currency all ready to go.

Central Bank Digital Currency (CBDC)—fiat currency issued by central banks in digital form—has progressed in the past few years from a bold speculative concept to a seeming inevitability. More than 80% of central bank respondents to a Bank for International Settlements survey in 2019 reported engagement in CBDC projects. Banks are planning but not telling their depositors what they have in mind.

How will small business compete?

To survive, business consultants say nearly every company will have to be a financial services company. Uber and Lyft now provide financial services for their drivers, creating in-house bank accounts so it can immediately pay drivers as they earn money. What is not said is that Uber and Lyft essentially get to keep some of their workers’ money on account, never leaving their bank and using their workers’ money without any return. It’s kind of like working for the coal mine and being forced to buy from the company store.

The Future of Banking Is … You’re Broke

Our present financial ruin is being turned

into a business model. – Molly Wood, WIRED

Molly Wood, writing at WIRED.com, says:Our present financial ruin is being turned

into a business model. – Molly Wood, WIRED

“Our present financial ruin is being turned into a business model.” In her discourse entitled THE FUTURE OF BANKING IS . . . YOU’RE BROKE,” she writes: “Seventy-eight percent of Americans live paycheck to paycheck. . . there is the

idea that the solution to our financial woes can be found in a more

convenient, higher-tech, friendlier-named digital bank.

The economy is sick and digital money is part of the problem, not the solution

A second problem is more serious.

Ultimately, no amount of friendly design, accessible features, and

overdraft protections will solve the underlying problems that made these

services necessary in the first place. No neo-bank can erase the

student loan debt or the 40-year stagnation in wages or the unexpected

medical expenses or the crippling reality of America’s existential

brokeness. The neo-banks have promised that they’ll ease your pain, but

that’s just morphine for the real condition. When it comes to the actual

sickness, you’re still on your own.”

No comments:

Post a Comment