Jack Mullen, BANKS GOING BUST, AMERICANS ON THE HOOK AS BANKERS PREPARE CBDC FOR LAUNCH |

Jack Mullen

As I have explained since June of last year, the banking system in the United States is not a creation of the Constitution, and it does not belong in any way to the people.

The monetary system and the banking networks that support that system are privately owned, employing privately owned copyrighted dollar bills adorned with secret society symbols and powered by lucrative privately patented technology. Dollar bills are Federal Reserve Notes, not United States Treasury Notes.

The Federal Reserve and NOT publicly elected officials and agencies of the US Government own,

direct, and operate the private, for-profit corporation engaged in controlling and managing the United States monetary system, creating and issuing debt as money, and issuing bills of credit – all of which are expressly unconstitutional.Keeping in mind the Federal Reserve is a private banking corporation serving the interests and goals of the corporation, it should be clear to most now that these interests and goals have turned to the destruction of the present dollar-based system and its private money transactions that do not involve the knowledge and are outside the control of the Federal Reserve system.

Echos Of Banking Collapses Past

European bankers and their brethren from Babylon had tirelessly attempted to create a central banking system in the United States since 1791. Thomas Jefferson fiercely opposed the First Bank Of the United States. Still, his warnings were trumped by Hamilton’s 15,000 words of support, which were enough to convince President George Washington to sign the first version of the Federal Reserve into law.

When the bank’s 20-year charter expired, the bank’s charter was not renewed. However, due to the war of 1812, a new 2nd National Bank of the United States was created to fund war debts, for which it failed miserably. During its twenty-year charter, bank activity was riddled with fraud and controversy.

In 1819 the bank was challenged as unconstitutional, and the famous case McCulloch vs. Maryland resulted in a decision favoring the bank by carefully narrowing the interpretation of the Constitutional government’s relationship with the bank. Instead of deciding whether Congress had the power to directly or indirectly emit bills of credit or otherwise convert debt into money – the court focused on the narrow question of whether or not the bank was a “necessary and proper” means for Congress to execute any “other” constitutional powers it might have [ibid].

Under that narrow interpretation and ignoring that the bank was issuing bills of credit and converting debt into money, the bank was deemed constitutional.

In 1828 Andrew Jackson was elected president, and the subject of the National Bank was back on the table. Jackson devoted his second term as president to ridding the nation of a national bank and restoring control of credit and banking to the Federal government and the States.

During that time, Jackson exposed the bank with eloquent speeches and then, at almost the cost of his life, began a war against the bank, which consumed his second term ending in the bank’s charter not being renewed. During that period, there was an attempt on his life which, as fate would have it, resulted in the misfiring of two guns, leaving Jackson unharmed. Jackson attacked his assailant with his cane, yelling, Let me alone! Let me alone! I know where this came from.

Jackson made one of the most passionate speeches ever heard in Congress, explaining his veto of a measure that would renew the national bank’s charter before expiring.

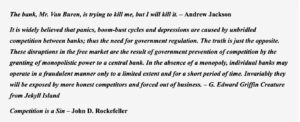

Is there no danger to our liberty and independence?…Will there not be cause to tremble for the purity of our elections in peace and for the independence of our country in war? …Should the stock of the Bank principally pass into the hands of the subjects of a foreign country, and we should unfortunately become involved in a war with that country, what would be our condition? Of the course which would be pursued by a bank almost wholly owned by the subjects of a foreign power, and managed by those whose interests, if not affections, would run in the same direction, there can be no doubt. All its operations within would be in aid of the hostile fleets and armies without. Controlling our currency, receiving our public moneys, and holding thousands of our citizens in dependence, it would be more formidable and dangerous than the naval and military power of the enemy….– Andrew Jackson [ibid] [emphasis JM]

Jackson prevailed after a long bitter fight with members of the bank and congress under the bank’s control and the Rothchild money that powered it.

In the previous years of the central bank, before its charter lapsed, total money in circulation had risen by eighty-four percent in just four years[ibid]. This money was contracted and removed when the central bank was forced to close.

The central bank’s money was created out of thin air, and when it was removed, 16% of the nation’s money supply was gone in just the first year.

Just like today, when the American dollar has finally reached hyperinflation because of central banks and banks collapsing from liquidity failure, the liquidity crisis of 1837 caused bank runs, unemployment, bankruptcy, and more.

The Panic of 37 became another rallying point for bankers claiming the hardships were not caused by the bank but rather by Jackson and his determination to end the bank. Much like today, we are told that this financial crisis resulted from inflation, but in reality, inflation is caused by central banking.

Between Andrew Jackson and 1907, two American Presidents, Garfield, and McKinley, were assassinated – both were ardently opposed to central banking, and much has been written about how their opposition to a new central bank led to their murders.

1907 Banking Crisis

By 1907 the central bankers were ready to once again create an engine of wealth for the bankers and their agenda worldwide by harnessing surreptitiously stolen American wealth. So as before, the method of gaining access to the free creation of American money was to cause the great bank runs of 1907. As usual, this meant bank runs, a stock market collapse, bankruptcies, and more pain and turmoil for the American public.

Unfortunately, Andrew Jackson was long gone. At that time, the people of America were as insulated from the truth then as they are today, so when they were told the US Government was creating a new banking system to protect people from banking predatory fraud, calamity, theft, and manipulation, they believed the Federal Reserve would be a Federal Agency and not a private banking cartel working for its own interests without over site or even the ability to be audited.

The name Federal Reserve was a deception designed to cloak the bankers behind the deal (swindle.)

And so there was a national movement to reform banking; the biggest banks, especially in New York, which dominated the whole scene, decided – they themselves would get at the head of the parade, that iconic meeting that took place on Jekyll Island, which was a private club in Georgia, where all of these bankers went to get out of the public eye. There are very few wars in history that were launched under conditions of greater secrecy. They created the central bank or the Federal Reserve System in secret because if the public had known that the reform legislation was written by the bankers, they would never have gone for it. The Federal Reserve System is a cartel of banks. They bring the politicians into it, and they pass it into law, and they call it reform and make it look like they’re serving the people because the government’s involved when in fact, the governments are serving the private interest. Right. So now you and I have to abide by the rules of the cartel, or we go to prison. We become indentured servants to the system. How much of our lives do we spend earning money that goes to taxes and interest on loan on money that didn’t even exist? This is a system of the banks for the banks by the banks and other banks. – (video) G. Edward Griffin: The Federal Reserve System

A Butterfly In Brazil Brings Does Not Cause A Tornado in California

The Butterfly Effect and strange attractors are unnecessary when looking for how bankers create financial instability before seeking to bring on the next parasitic banking model. This can be summed up with the well-documented theory of Problem, Reaction, and Solution.

The opening salvo of a soon-to-be domino banking collapse began with Silicon Valley Bank (SVB) after a stunning 48 hours in which a bank run and a capital crisis led to the second-largest failure of a financial institution in US history.

According to John Perkins, author of Economic Hit Man: HitMen are highly paid professionals who cheat countries around the globe out of trillions of dollars. Their tools include fraudulent financial reports, rigged elections, payoffs, extortion, sex, and murder.

SVB was the targeted straw that broke the camel’s back. Much like the economic hitmen described by John Perkins, Moody’s financial ratings service started the bank panic and runs by notifying and downgrading Silicon Valley Bank of the problems they appeared not to have noticed.

Lest you have forgotten – Moody’s and Standard and Poor’s were both involved in the financial crisis of 2008, and both were shown to have had a part in causing the crisis resulting in the looting of $16 Trillion by the banks and associates.

Ratings agency Moody’s has agreed to pay nearly $864 million in a settlement with the US authorities over its inflated ratings of risky mortgage securities that contributed to prompting the 2008 global financial crisis…[ibid]

In the case above, Moody’s provided fraudulent ratings on mortgage-backed securities – but there is no reason they cannot be used to cause a run on a bank leading to bankruptcy, leaving the bank open for vulture bankers to pick up the valuable assets while leaving the losers and the total losses for the American public deal with.

SVB collapse: HSBC buys Silicon Valley Bank’s UK branch for just over $1

Moody’s may have been used to deliberately downgrade nations like Greece in 2010 or South Africa in 2019. After Moody’s downgraded South Africa’s credit rating in 2019, foreign investors took advantage of the situation by buying up South African assets at discounted prices, increasing profits for the investors while putting downward pressure on the South African economy.

On Tuesday, Moody’s cuts outlook on U.S. banking system to negative, citing ‘rapidly deteriorating operating environment.

SVB Anomalies

A few anomalies associated with SVB will need further investigation as to what really happened.

The bank’s president and chief executive, Gregory Becker, was a former Federal Reserve Board Member serving at the San Francisco fed who coincidentally sold $3.6 million in SVB shares stock just two weeks earlier. Two other executives are said to have sold their shares, bringing the total to over $5 million after the sales were finalized.

Also interesting is that the bank paid out its 2022 bonus package coincidentally on the same day, hours before it collapsed.

Further, the cause of the bank’s illiquidity was said to be rising interest rates which had devalued the bank’s investment in Mortgage Backed Securities and treasuries putting the balance sheet in peril. On the public side, during the weeks before the collapse, depositors, feeling the financial pain of rising interest rates and simultaneous inflation, began to remove funds from their accounts. But..

Here’s the rub – A former fed bank director is no rookie. Clearly, the bank’s investments in interest-rate-sensitive assets would have sounded general alarms months and months ago.

At the same time, a seasoned fed bank director would already understand that quickly raising interest rates as the Federal Reserve has been doing over the past year will create liquidity problems for all banks in general. Further, with rising interest rates and inflation, naturally, deposits would begin to be removed. This is banking 101 material and leaves me wondering how this well-funded bank in 2022 ended up being the first causality in the banking collapse of 2023.

Another interesting event signaling advance warning of the imminent collapse was Peter Thiel’s Founders Fund got its cash out of Silicon Valley Bank before it was shut down,

I will leave this analysis for now and provide my closing thoughts at the end of this article. But we can say that given the history of central banking and the enormous financial losses, pain, bankruptcy, job losses, and looting seen over the history of central banking. SVB’s failure, and the consequences, is not a random event – it’s no butterfly effect.

Special Statement On Banks

As we have shown, but in very little detail, banks have been the source of uncountable losses, bankruptcies, fortunes lost, pain, deception, and in many cases, murder. The central bank is an industry of theft covered with an exterior of safety, security, large columns, and heavily guarded vaults. But these vaults are usually empty, just like their promises.

When banks win, they keep the profit, but when they lose, the people pay the losses.

As I said in a previous issue, banks are failing now and will transfer their losses to depositors using the contract notion of the “unsecured creditor.” Banking contracts with depositors give them the right to reach into your account and take your money to prevent their losses from closing the bank.

Furthermore, awake people are taking their money out of banks to prevent their earnings from being stolen, causing extensive and unpublicized bank runs.

Bank runs are a sign that a bank might soon fail.

Please don’t wait for your bank to experience a run; they happen very fast, often overnight or over the weekend. Be safe, take precautions, and get your money out of banks and into the safety of something tangible. Keep only what you need in the bank and utilize the rest to prepare for what is coming next.

Market Report

Federal Reserve Announces Fantastic Bank Bailout.

As expected, the Federal Reserve will rescue many of its crony banks, and the American public will pay the bill. Just like in 2008 we can expect not a single banker to go to jail.

They call this bailout a liquidity injection, but a rose by any other name is still a rose. This injection will directly cause more inflation, and that inflation will devalue your dollars more and more every day. Rather than closing banks and clearing the debt through standard bankruptcy proceedings, the criminal banks will remain alive, and even though they are getting up to $2 Trillion, they will not remain liquid, this is just the first round of bank bailouts: we are witnessing the final collapse of the current banking system.

The American public’s economic climate worsens as the banks get bailed out. Interest rate hikes will continue, and inflation is still rising. These two factors alone mean more and more banks will become insolvent. Banks depend on selling loans, holding deposits, and raking in fees. But Americans are removing their deposits to live on now and fewer people can support new loans – leaving them to drown in a self-created quagmire.

Market Summary

Money Supply Rising

Following the trail of inflation, Basic-M1 (curreny + demand deposits) reached a 52 year high and was 120% higher than February 2020 (beginning of plandemic.) A rising money supply is a key component causing inflation.

Construction and Housing

January 2023 Real Construction Spending posted its 17th straight month of year-to-year decline. Those numbers are adjusted for inflation, using the Construction Producer Price Index. This pattern remains consistent with a deepening, albeit not formally recognized Economic Recession. [Ibid]

Flight to Metals and Bitcoin

Gold, Silver rise, and Bitcoin is over $26,000. Universally recognized monetary metals are rising as inflation continues upward. At the same time the fed announced another multi-trillion dollar criminal bank bailout – pure inflation.

The final call for low-price access to monetary metals has been given. This opportunity window will close sometime later this year.

Bitcoin is will continue to move upwards, with higher lows and higher highs as the dollar’s purchasing power continues to fall.

US Manufacturing Nose Dives

US factory orders fall as civilian aircraft demand dives.

Airlines are struggling to find pilots that have not been affected by the covid-19 vaccine while pandemic restrictions on airlines squashed demand

According to U.S. Labor Department, core inflation continued at 0.5% in February.

Silver and gold are still on sale now: make sure to take advantage of this sale.

A Commodity SUPER-SPIKE Is Coming. Are You Ready for It?

Bankers preparing for the demise of the dollar: Central Banks Are Buying Gold At The Fastest Pace In 55 Years

Today commodities, in general, are in massive INVERSE bubbles; therefore, when risk-on eventually becomes risk-off, and it will, the price of commodities will SUPER-SPIKE.

Silver demand reached an all-time high in 2022, according to the Silver Institute.

Demand for silver was expected to have reached a new high of 1.21 billion ounces in 2022, up 16 percent from the year before, driven by increases in industrial use, jewelry and silverware offtake, and physical investment.

Mining stocks are beginning to come alive, and giant companies like BHP are reporting record-high earnings and stock prices. Junior mining stocks are at the launch pad and judiciously choosing the right company might be your key to banker independence over the next few years.

Demand for Silver will continue to increase this year.

Silver Spot Price: $22.80 | 1 oz. Silver Eagle Price $35.08 | Premium 53.85% ↓

Gold Spot Price: $1992.65 | 1 oz. Gold Eagle Price $2,185.65 | 9.68% ↑

$50 face value junk silver $1,202.50 | 47.45% over spot price for 71.5% silver quarters ↑

10 Yield: 3.395% [UNSTABLE! And Hard To Manage Now]↓

Bitcoin $26,781.00 ↑

Crude Oil Price: $66.41 ↓

* note arrows show price increase or decrease over the last article.

Final Thoughts

Since the late 18th century, central banking has been at war against the American people. Central bankers are international and live in a parallel civilization with no allegiances or loyalty to any nation, political system, or morality. Bankers have historically built up nations to steal wealth and steer their world conquest goals and agenda toward the future, using other people as the power source. Then after leaving a country drained and destitute, they pack up and move to another.

In America, the bankers ran into resistance from great men like Thomas Jefferson and Andrew Jackson, James Garfield, Abraham Lincoln, William McKinley, John F. Kennedy, and others. These men were sometimes successful and other times assassinated in the war to prevent a parasitic system of insidious slavery disguised as a necessary and better way of banking in the United States.

We are now faced with the collapse of the United States, bankers having siphoned the wealth of the world’s most productive nation slowly for 120 years in a row. Soon after attaching themselves to the core of American wealth, they began to involve the country in wars starting with World War 1 just 4 years later.

Life in the United States never got better during the years of banker occupation. The nation was pushed into one war after another. In contrast, its currency, the financial lifeblood of the country, continued to purchase less and less, having today lost nearly 98% of its purchasing power since its replacement of the Constitutional currency in 1914.

American families were targeted causalities in this war. Once, it took only one family member to work out of the house while the other – usually a mother – maintained the home.

This same group targeted education, and now the children of the United States rank 10th overall in high school literacy education.

This interview with a former congressional staff researcher investigating tax-exempt foundations is a fantastic explanation of how the family and education system were deliberately destroyed. The same Norman Dodd had this to say about the Federal Reserve

I have shown in previous articles that World Wars are only likely or even possible with central banking. Coincidentally, bankers benefit from war via interest on loans to the warring nations. It is well known that bankers fund both sides of world wars, and in the end, they are the only victors.

The SVB collapse and the lost confidence in banking it created is only the beginning. As in 1907, today’s banking collapses are deliberate and generally caused by purposeful financial fraud benefiting bankers and their cronies while defrauding depositors, shareholders, and bondholders.

The purpose of which is long-term destabilization through long-term debt creation. Over the appropriate time, the banking system becomes insolvent – its losses are paid for by more public debt (the people.) Eventually, on schedule, the debt becomes so large it cannot be sustained, and the entire financial system becomes illiquid and collapses. We are reaching this point.

The time has come to make your final plans to survive the collapse, as it will cause a significant loss of life. Then, it is imperative that we forcefully, if necessary, refuse to participate in any further central banking swindle.

The Central Bank Digital Currency or any other introduction of a new system by the central banking cartels must be rejected.

Failure to reject and eliminate all attempts to create a central banking system in the future will result in a new form of slavery that will be nearly impossible to escape.

Please educate yourself, take action to secure your future, and strengthen your mind with knowledge about what is being planned. It is not possible to resist the next form of slavery unless you understand the consequences of accepting a new financial system created and controlled by the very same destroyers that have caused most of the wars, hardships, and poverty of the past 120 years.

To prepare the nation to accept the new Central Bank Digital Currency, we should expect to hear more and more about the failures of the current system and the need to replace it with something better, safer, and not prone to bank runs or bank liquidity issues.

Today I saw an article claiming that Elon Musk was making cryptic comments about the current banking crisis in a tweet.

The inefficiency of the set of heterogeneous resource allocation databases we call money is astounding. – Elon Musk Tweet

The article said that he believed that what Musk said might mean that it would probably be easier to have a central entity where customers can deposit and withdraw money, rather than a system with multiple entry and exit points. The more points of entry and exit you have, the greater the risk of failure, he might suggest.

Musk was signaling to his peeps that a central banking system without individual banks (heterogeneous resource allocation databases) would be a far better idea. I am pretty confident Musk believes the CBDC would be more efficient.

Eventually this creature is going to grow and grow and grow and get a bigger portion of our lives until finally they have it all. Unless we change this system. We have a wonderful opportunity with the tools of communication that we have. We can create a movement to actually reverse this because if we don’t win this war, it won’t will make any difference we lose everything. So we have no option. We have to fight and we have to win – American Hero G. Edward Griffin

Here are a few things of immediate importance.

Move out of cities.

Convert dollars that will be held hostage in the banking system to silver (and gold).

Keep Enough cash on hand for a month of typical requirements.

Keep stocking up on food.

Purchase and stockpile items for barter in times when money is not accepted.

Purchase productive assets (farms, farmland, tractors, specialized machinery).

Make preparations for gasoline and diesel fuel shortages coming this winter.

Obtain necessary components of cooking – cooking oils, flour, sugar, seasonings, etc.

Learn new skills: fishing, hunting, food storage, and gardening.

Purchase a water purification system.

Home cooking supplies, including fuel for stoves.

Medical supplies for humans and animals

Invest in solar equipment for power generation.

Consider communications a priority and invest in radio equipment (shortwave receivers, shortwave radios (get your license), GMRS radios.

Preparation Over Fear!

No comments:

Post a Comment